Filing

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of

The Securities Exchange Act of 1934

April 27, 2017

Date of Report (Date of earliest event reported)

SAVARA INC.

(Exact name of registrant as specified in its charter)

| Delaware | 001-32157 | 84-1318182 | ||

| (State or other jurisdiction of incorporation) |

(Commission File Number) |

(I.R.S. Employer Identification No.) |

900 Capital of Texas Highway

Las Cimas IV, Suite 150

Austin, Texas 78746

(Address of principal executive offices)

(512) 961-1891

(Registrant’s telephone number, including area code)

Mast Therapeutics, Inc.

3611 Valley Centre Drive, Suite 500

San Diego, California 92130

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

| ☐ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§ 230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§ 240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Table of Contents

Item 2.01. Completion of Acquisition or Disposition of Assets.

On April 27, 2017, Mast Therapeutics, Inc. (the “Company”), completed its business combination with Savara Inc., which changed its name in connection with the transaction to “Aravas Inc.” (“Savara”), in accordance with the terms of the Agreement and Plan of Merger and Reorganization, dated as of January 6, 2017, by and among the Company, Victoria Merger Corp. (“Merger Sub”), and Savara (the “Merger Agreement”), pursuant to which Merger Sub merged with and into Savara, with Savara surviving as a wholly owned subsidiary of the Company (the “Merger”).

Also, on April 27, 2017, in connection with and immediately prior to the effective time of the Merger (the “Effective Time”), the Company (i) effected a reverse stock split at a ratio of one new share for every 70 shares of its common stock outstanding (the “Reverse Stock Split”), and (ii) changed its name to “Savara Inc.” Following the completion of the Merger, the business conducted by the Company became primarily the business conducted by Savara, which is a clinical-stage specialty pharmaceutical company focused on the development and commercialization of novel therapies for the treatment of serious or life-threatening rare respiratory diseases.

Under the terms of the Merger Agreement, the Company issued shares of its common stock to Savara’s stockholders, at an exchange ratio of 0.5860 of a share of common stock (post Reverse Stock Split), in exchange for each share of Savara common stock outstanding as of the Effective Time. The Company also assumed all of the stock options issued and outstanding under the Savara 2008 Stock Option Plan (the “Savara Plan”) and issued and outstanding warrants of Savara, with such stock options and warrants henceforth representing the right to purchase a number of shares of the Company’s common stock equal to 0.5860 multiplied by the number of shares of Savara’s common stock previously represented by such stock options and warrants, as applicable.

Immediately following the Effective Time, there were approximately 15.1 million shares of the Company’s common stock outstanding (post Reverse Stock Split). Immediately following the Effective Time, the former Savara stockholders, warrantholders and optionholders owned approximately 77% of the Company, with the Company’s stockholders, warrantholders and optionholders immediately prior to the Merger, whose warrants, options and shares of the Company’s common stock remain outstanding after the Merger, owning approximately 23% of the Company.

The issuance of the shares of the Company’s common stock to the former stockholders of Savara was registered with the U.S. Securities and Exchange Commission (the “SEC”) on a Registration Statement on Form S-4 (Reg. No. 333-216012) (the “Registration Statement”). The issuance of the shares of the Company’s common stock to holders of stock options issued, or to be issued, under the Savara 2008 Stock Option Plan will be registered with the SEC on a Registration Statement on Form S-8. The Company’s shares of common stock, which were previously listed on NYSE MKT, LLC and traded through the close of business on April 27, 2017 under the ticker symbol “MSTX,” will commence trading on The Nasdaq Capital Market (“Nasdaq”), under the ticker symbol “SVRA” on April 28, 2017. The Company’s common stock has a new CUSIP number, 80511Q 106.

The descriptions of the Merger and Merger Agreement included herein are not complete and are subject to and qualified in their entirety by reference to the Merger Agreement, a copy of which was attached as Exhibit 2.1 to the Company’s Current Report on Form 8-K filed with the SEC on January 9, 2017 and incorporated herein by reference.

On April 27, 2017, the Company issued a press release announcing the completion of the Merger. A copy of the press release is attached hereto as Exhibit 99.1.

Item 2.02 Results of Operations and Financial Condition.

Following the closing of the Company’s business combination with Aravas (formerly known as Savara Inc.) on April 27, 2017 and the payment of severance amounts to former employees and certain transaction related expenses, the Company’s balance of cash, cash equivalents and investment securities was approximately $16 million. This cash balance includes approximately $4 million in aggregate proceeds from the exercise of certain previously issued warrants to purchase Aravas shares and additional capital invested into Aravas prior to the closing of the business combination.

The information in this Item 2.02 shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that Section, nor shall it be incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such filing.

2

Table of Contents

Item 3.03. Material Modification to Rights of Security Holders.

To the extent required by Item 3.03 of Form 8-K, the information contained in Item 2.01 of this Current Report on Form 8-K is incorporated by reference herein.

On April 27, 2017, immediately prior to the Effective Time, the Company amended and restated its certificate of incorporation to (i) effect the Reverse Stock Split and (ii) change the Company’s name to “Savara Inc.” The amendment and restatement of the Company’s certificate of incorporation was approved by the Company’s stockholders at a special meeting of its stockholders on April 27, 2017.

The foregoing descriptions of the Company’s amended and restated certificate of incorporation are not complete and are subject to and qualified in their entirety by reference Company’s amended and restated certificate of incorporation, a copy of which is attached as Exhibit 3.1 hereto and is incorporated herein by reference.

3

Table of Contents

Item 5.01. Changes in Control of Registrant.

The information set forth in Item 2.01 of this Current Report on Form 8-K is incorporated by reference into this Item 5.01.

In accordance with the Merger Agreement, on April 27, 2017, effective as of the Effective Time, Howard C. Dittrich, Peter Greenleaf, and Brian M. Culley resigned from the Board and any respective committees of the Board to which they belonged, Matthew Pauls resigned from his position on the audit committee and nominating and governance committee, and David Ramsay resigned from his position on the nominating and governance committee. The Board appointed, effective as of the Effective Time, Robert Neville, Nevan Elam, Richard J. Hawkins, Joseph S. McCracken and Yuri Pikover as directors of the Company whose terms expire at the Registrant’s next annual meeting of stockholders.

Item 5.02. Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers.

(b) Pursuant to the Merger Agreement, on April 27, 2017, effective as of the Effective Time, Howard C. Dittrich, Peter Greenleaf, and Brian M. Culley resigned from the Board and any respective committees of the Board on which they served, which resignations were not the result of any disagreements with the Company relating to the Company’s operations, policies or practices.

Also, pursuant to the Merger Agreement, on April 27, 2017, effective as of the Effective Time, the Company terminated the employment of Brian M. Culley, the Company’s Chief Executive Officer, Brandi L. Roberts, the Company’s Chief Financial Officer and Senior Vice President, Edwin Parsley, the Company’s Chief Medical Officer and Senior Vice President, and Shana Hood, the Company’s General Counsel, Vice President and Secretary. In connection with the termination of the employment, such officers resigned all of the positions they held with the Company and its subsidiaries.

(c) Effective as of the Effective Time, the Company’s board of directors appointed Robert Neville as the Company’s Chairman and Chief Executive Officer, Taneli Jouhikainen as the Company’s President and Chief Operating Officer, and David Lowrance as the Company’s Chief Financial Officer. There are no family relationships among any of the Company’s directors and executive officers. The information set forth in Item 8.01 of this Current Report on Form 8-K regarding the biographical information, compensation arrangements and related party transaction information for the newly appointed executive officers of the Company is incorporated by reference to this Item 5.02(c). Each of the newly appointed executive officers of the Company entered into the Company’s standard form of indemnification agreement with the Company on April 27, 2017, the form of which is attached hereto as Exhibit 10.12 and incorporated herein by reference.

(d) The information set forth in Item 5.01 of this Current Report on Form 8-K with respect to the appointment of directors to the Company’s board of directors pursuant to and in accordance with the Merger Agreement is incorporated by reference into this Item 5.02(d). The information set forth in Item 8.01 of this Current Report on Form 8-K regarding the related party transaction information for the newly appointed directors of the Company is incorporated by reference to this Item 5.02(d). Each of Nevan Elam, Richard J. Hawkins, Joseph S. McCracken and Yuri Pikover entered into the Company’s standard form of indemnification agreement with the Company on April 27, 2017, the form of which is attached hereto as Exhibit 10.12 and incorporated herein by reference.

4

Table of Contents

Audit Committee

On April 27, 2017, Yuri Pikover and Richard Hawkins were appointed to the audit committee of the Board. David Ramsay will continue to serve as the chairman of the audit committee.

Compensation Committee

On April 27, 2017, Nevan Elam and Joseph McCracken were appointed to the compensation committee of the Board, and Nevan Elam was appointed as the chairman of the compensation committee. Matthew Pauls will continue to serve on the compensation committee.

Nominating and Corporate Governance Committee

On April 27, 2017, Yuri Pikover, Nevan Elam and Joseph McCracken were appointed to the nominating and corporate governance committee of the Board, and Yuri Pikover was appointed as the chairman of the nominating and corporate governance committee.

Item 5.03 Amendments to Articles of Incorporation or Bylaws; Change in Fiscal Year.

(a) To the extent required by Item 5.03 of Form 8-K, the information contained in Item 2.01 and Item 3.03 of this Current Report on Form 8-K is incorporated by reference herein.

Item 5.07 Submission of Matters to a Vote of Security Holders.

On April 27, 2017, the Company held a special meeting of stockholders (the “Special Meeting”) to consider five proposals related to the Company’s previously announced merger with Savara, pursuant to the Merger Agreement. Each of the Company’s proposals was approved by the requisite vote of the Company’s stockholders as described below. The closing of the merger and the related transactions contemplated by the Merger Agreement are currently expected to be completed on or around April 27, 2017.

At the close of business on March 13, 2017, the record date for the Special Meeting, the Company had 254,746,933 shares of common stock issued and outstanding. The holders of a total of 141,518,037 shares of common stock were represented at the Special Meeting by proxy, representing approximately 55.55% of the Company’s issued and outstanding common stock as of the record date, which total constituted a quorum for the Special Meeting in accordance with the Company’s bylaws.

The approval of the Merger Agreement and the issuance of the Company’s common stock pursuant to the Merger Agreement (Proposal No. 1) required the affirmative vote of the holders of a majority of the shares of the Company’s common stock having voting power present in person or represented by proxy at the Special Meeting. The approval of the 1:70 reverse stock split and the change of the Company’s corporate name (Proposal Nos. 2 and 3, respectively) required the affirmative vote of the holders of a majority of the shares of the Company’s common stock having voting power outstanding on the record date for the Special Meeting. The approval of the 1:70 reverse stock split was required in order to authorize the Company’s issuance of the shares of its common stock pursuant to the Merger Agreement and allow for the listing of the common stock of the combined company on the NASDAQ Stock Market following the closing of the merger. As a result, each of Proposal Nos. 1, 2 and 3 were conditioned on each other and, therefore, each was required to pass in order for the merger and the other transactions contemplated by the Merger Agreement to be consummated. The approval, on a non-binding advisory vote basis, of the compensation that will or may become payable by the Company’s to its named executive officers in connection with the merger (Proposal No. 4) and the approval of the adjournment of the Special Meeting, if necessary, to solicit additional proxies (Proposal No. 5) required the affirmative vote of the holders of a majority of the shares of the Company’s common stock having voting power present in person or represented by proxy at the Special Meeting.

The final voting results for each of these proposals is set forth below. Brokers did not have discretionary authority to vote for Proposal Nos. 1, 2, 3 and 4 for the shares of the Company’s common stock held in street name, and as a result, no broker non-votes were received for any of these proposals. For more information on these proposals, please refer to the Company’s prospectus/proxy statement/information statement for the Special Meeting, filed with the Securities and Exchange Commission on March 15, 2017.

5

Table of Contents

Proposal 1. To adopt and approve the Merger Agreement, and to approve the merger and the issuance of the Company’s common stock pursuant to the Merger Agreement:

| 136,743,223 For | 2,208,399 Against | 2,566,415 Abstain | 0 Broker Non-Votes |

Proposal 2. To approve the amended and restated certificate of incorporation of the Company to effect a reverse stock split of the Company’s common stock, at a ratio of one new share for every 70 shares outstanding:

| 131,209,899 For | 6,929,240 Against | 3,378,898 Abstain | 0 Broker Non-Votes |

Proposal 3. To approve the amended and restated certificate of incorporation of the Company to change the name “Mast Therapeutics, Inc.” to “Savara Inc.”:

| 136,330,701 For | 2,328,118 Against | 2,859,218 Abstain | 0 Broker Non-Votes |

Proposal 4. To approve, on a non-binding advisory vote basis, compensation that will or may become payable by the Company to its named executive officers in connection with the merger:

| 112,373,749 For | 23,589,121 Against | 5,555,167 Abstain | 0 Broker Non-Votes |

Proposal 5. To adjourn the Special Meeting, if necessary, to solicit additional proxies if there are not sufficient votes in favor of Proposal Nos. 1, 2, 3 and 4 (although Proposal No. 5 was approved, adjournment of the Special Meeting was not necessary or appropriate because there were sufficient votes at the time of the Special Meeting to approve the other proposals):

| 127,075,022 For | 11,351,993 Against | 3,091,022 Abstain | 0 Broker Non-Votes |

Item 8.01 Other Events.

In connection with the Merger and related transactions described in this Current Report on Form 8-K, the Company provides the following information related to Savara set forth in this Item 8.01.

6

Table of Contents

7

Table of Contents

Cautionary Statement Concerning Forward-Looking Statements

The information in Item 8.01 of this Current Report on Form 8-K, particularly in the sections entitled “Savara Business,” and “Savara Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the information incorporated herein by reference, include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements are based on current expectations and beliefs and involve numerous risks and uncertainties that could cause actual results to differ materially from expectations. These forward-looking statements should not be relied upon as predictions of future events as we cannot assure you that the events or circumstances reflected in these statements will be achieved or will occur. When used in this report, the words “believe,” “may,” “could,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “indicate,” “seek,” “should,” “would” and similar expressions are intended to identify forward-looking statements, though not all forward-looking statements contain these identifying words. All statements, other than statements of historical fact, are statements that could be deemed forward-looking statements.

If any of these risks or uncertainties materializes or any of these assumptions proves incorrect, our results could differ materially from the forward-looking statements in this report. All forward-looking statements in this report are current only as of the date of this report. We do not undertake any obligation to publicly update any forward-looking statement to reflect events or circumstances after the date on which any statement is made or to reflect the occurrence of unanticipated events.

The Company was incorporated in Delaware in December 1995. In October 2000, the Company merged its wholly-owned subsidiary, Biokeys Acquisition Corp., with and into Biokeys, Inc. and changed its name to Biokeys Pharmaceuticals, Inc. In May 2003, the Company merged Biokeys, Inc., a wholly-owned subsidiary, with and into the Company and changed the Company’s name to ADVENTRX Pharmaceuticals, Inc. In March 2013, the Company merged Mast Therapeutics, Inc., a wholly-owned subsidiary, with and into the Company and changed the Company’s name to Mast Therapeutics, Inc. In April 2017, the Company merged its wholly-owned subsidiary, Victoria Merger Corp., with and into Aravas Inc. (formerly, Savara Inc.) and changed the name of the Company to Savara Inc.

8

Table of Contents

Savara is a clinical-stage specialty pharmaceutical company focused on the development and commercialization of novel therapies for the treatment of serious or life-threatening rare respiratory diseases. Savara’s pipeline comprises AeroVanc, a Phase 3 ready inhaled vancomycin, and Molgradex, a Phase 2/3 stage inhaled granulocyte-macrophage colony-stimulating factor, or GM-CSF. Savara’s strategy involves expanding its pipeline of best-in-class products through indication expansion, strategic development partnerships and product acquisitions, with the goal of becoming a leading company in its field. Savara’s management team has significant experience in orphan drug development and pulmonary medicine, in identifying unmet needs, creating and acquiring new product candidates, and effectively advancing them to approvals and commercialization.

AeroVanc, an inhaled formulation of vancomycin, is being developed for the treatment of persistent methicillin-resistant Staphylococcus aureus, or MRSA, lung infection in cystic fibrosis, or CF, patients. CF is a genetic disease that involves sticky mucus buildup in the lungs, persistent lung infections and permanent and progressive respiratory disability. There are approximately 30,000 patients affected by CF in the United States, and MRSA infection has become increasingly common in these patients, with a prevalence of approximately 26%. Persistent MRSA infection in CF patients is associated with increased use of intravenous, or IV, antibiotics, increased hospitalizations, a faster decline of lung function, as well as shortened life-expectancy. Due to the lung pathology associated with CF, persistent MRSA lung infection is difficult to eradicate or manage using oral or IV antibiotics, and there is no standard of care to manage this condition. Whereas inhaled antibiotics have become a cornerstone of treating the most prevalent chronic pathogen in CF patients, Pseudomonas aeruginosa, there are no approved inhaled antibiotics addressing MRSA lung infection. In a randomized, double-blind, placebo-controlled Phase 2 study in CF patients with persistent MRSA infection, AeroVanc met a primary endpoint to reduce MRSA density in sputum, and showed encouraging trends of improvement in lung function, and respiratory symptoms, as well as prolongation of the time to use of other antibiotics, with best responses in subjects under 21 years of age. After receiving detailed guidance from the FDA, Savara has planned a pivotal Phase 3 study of AeroVanc that it anticipates starting in the third quarter of 2017.

Molgradex, an inhaled formulation of recombinant human GM-CSF, is being developed for the treatment of autoimmune pulmonary alveolar proteinosis, or PAP, a rare lung disease characterized by the build-up of lung surfactant in the alveoli, or air sacs, of the lungs. PAP is estimated to have a prevalence of approximately 2,500 patients in the United States. The disease process underlying PAP involves an autoimmune response against a naturally occurring protein, GM-CSF, suppressing the stimulating activity of GM-CSF on lung macrophages which function to clear excess surfactant from the alveoli. The best treatment currently available for PAP is a procedure called whole lung lavage, or WLL, which entails washing out the lungs bronchoscopically with saline, segment by segment, under general anesthesia. By its nature, WLL is an invasive and inconvenient procedure that requires hospitalization, and highly experienced physicians at specialist sites. Based on published investigator-sponsored treatment experience with inhaled GM-CSF, Savara believes Molgradex has the potential to replace the inactivated GM-CSF in PAP patients, and thereby to restore the surfactant clearing activity of the alveolar macrophages, and to become the treatment of choice for PAP. The company has completed a Phase 1 study in healthy volunteers, and is currently conducting a pivotal Phase 2/3 study in Europe and Japan, with top line results expected in the first quarter of 2018.

9

Table of Contents

Savara’s pipeline of product candidates is illustrated in the figure below. In order to fully exploit the potential of its current pipeline, Savara is also pursuing indication expansions of its product candidates, with priority on the development of Molgradex in rare infectious lung diseases, where stimulation of the innate immune system has the potential to improve clinical outcomes. Savara is planning to advance the first such Molgradex indication expansion program into clinical Phase 2 development during 2017, and plans to disclose further information about the program throughout 2017.

Savara’s product candidate pipeline

Savara currently owns exclusive worldwide rights to its product portfolio, except in Japan where rights to Molgradex have been licensed out to Nobelpharma Co., Ltd. AeroVanc has been granted Orphan Drug Designation and Qualified Infectious Disease Product, or QIDP, status for the treatment of persistent MRSA lung infection in CF patients in the United States, and Molgradex has been granted Orphan Drug Designation for the treatment of PAP in the United States and the European Union. The Orphan Drug Designation makes AeroVanc and Molgradex eligible for seven years of exclusivity from approval in the United States, and ten years of exclusivity in the European Union, whereas the QIDP status makes AeroVanc eligible for an additional five years of exclusivity in the United States.

AeroVanc Key Advantages — Savara is currently preparing to initiate a Phase 3 clinical study of AeroVanc, to be conducted primarily in the United States and Canada. Savara has received detailed guidance from the FDA on the design of the study, and believes that the planned study is in accordance with the FDA’s requirements for a sole pivotal study to be submitted for NDA approval. Savara anticipates initiating the study in the third quarter of 2017. Savara believes the results from its Phase 2 study, illustrated in part below, support the use of the same key endpoints and advancing the development of AeroVanc into a larger pivotal Phase 3 study. Notably, the Phase 2 study demonstrated a trend of clinically meaningful improvement in FEV1, a common measure of lung function illustrated below on the left, as well as in time to use of another antibiotic for respiratory infection, illustrated below on the right. The planned primary efficacy endpoint of the Phase 3 study is change from baseline in FEV1, and the primary analysis population will comprise patients under the age of 21, in line with experience from earlier clinical studies of inhaled anti-pseudomonal antibiotics in CF.

10

Table of Contents

Change from baseline in FEV1 (left) and Time to use of other antibiotic for respiratory infection (right)

|

|

| |

| Per Protocol Population, 32 mg dose cohort, < 21 years of age, n = 16 | Intent-to-treat Population, 32 mg dose cohort, < 21 years of age, n = 20 | |

Savara believes that AeroVanc has a number of important characteristics that contribute to its clinical profile and clinical data to date, and that facilitate its regulatory approval and successful commercialization. Specifically, AeroVanc offers:

| • | Strong product foundation, applying a previously approved active substance and previously approved drug delivery technologies. |

| • | High concentration of antibiotic is delivered directly to the lungs, the primary site of infection, which Savara believes can result in higher clinical efficacy and reduced systemic toxicity, as compared with oral or IV delivery of antibiotics. |

| • | Capsule based powder inhaler providing a fast and convenient method of administration, which is very desirable in the CF population, who have a high treatment burden. |

| • | Eligible for strong market protection via orphan drug status, QIDP status, a formulation patent, and an exclusive device supply agreement. |

Molgradex Key Advantages — Savara is currently conducting a Phase 2/3 clinical study, which is referred to as the IMPALA study, of Molgradex in Europe and Japan. Savara has received guidance from the European Medicines Agency, or EMA, on the design of the study, and believes the ongoing study is in accordance with the EMA’s requirements for a sole pivotal study to be used in a marketing authorization application submission in the European Union. Savara anticipates reporting top-line results from the study in the first quarter of 2018. Savara is also in discussions with the FDA to receive guidance on the clinical study requirements for an NDA submission in the United States. Savara expects to have clarity on those requirements later this year. The options include expanding and modifying the ongoing IMPALA study as the sole pivotal study, or conducting a second pivotal study for US regulatory purposes.

Building upon the published investigator-sponsored treatment experience with inhaled GM-CSF, Savara believes Molgradex has the potential to become the treatment of choice for PAP. Molgradex has the following characteristics that Savara believes will contribute to its clinical profile, as well as facilitate its regulatory approval and successful commercialization. Specifically, Molgradex offers:

| • | Strong product foundation, applying a previously approved active substance class and previously approved drug delivery technology. |

| • | GM-CSF is delivered directly to the lungs, the primary site of macrophage function deficiency, which Savara believes can result in high clinical efficacy with limited systemic adverse effects. |

| • | High efficiency nebulizer providing a fast and convenient method of administration, which is highly desirable for long-term treatment in a chronic disease, such as PAP. |

11

Table of Contents

| • | Eligible for strong market protection via orphan drug status, a proprietary cell bank used in the production of the drug substance, and an exclusive device supply agreement. |

Savara’s goal is to become a leading specialty pharmaceutical company focused on treatments for rare respiratory diseases, through the development and commercialization of novel and best-in-class therapeutics to address unmet medical needs in its field. The key elements of Savara’s strategy include:

| • | Pursue AeroVanc and Molgradex indication expansion. While Savara’s immediate priority is to obtain regulatory approvals in the primary indications described above, Savara believes both AeroVanc and Molgradex have the potential to be used for the treatment of several other diseases. In particular, Savara is exploring the use of Molgradex for the treatment of certain rare infectious lung diseases. |

| • | Expand the product pipeline through strategic product acquisitions. In addition to broadening its current pipeline through indication expansion, Savara’s strategy includes expansion of its product pipeline through strategic partnerships and product acquisitions, such as its acquisition of the Molgradex program through the asset purchase of Serendex Pharmaceuticals in 2016. A key priority has been to exploit known chemical entities or classes in novel ways, such as delivery of drug directly into the lungs, for the treatment of serious or life-threatening lung diseases. While Savara has developed an internal core competence in inhaled drug development, the company is technology agnostic. Future pipeline expansion decisions will be based on the unmet medical need within a specific disease, the commercial opportunity, and the ability to rapidly develop and commercialize a product candidate. |

| • | Operate by outsourcing capital intensive operations. Savara plans to continue to pursue the development and manufacturing of its product candidates by outsourcing most clinical development and all manufacturing operations. Savara’s business model has facilitated rapid development of its pipeline by using high quality specialist vendors and consultants in a capital efficient manner. |

| • | Establish its own sales and marketing capabilities to commercialize its products in the United States. Savara plans to commercialize its pipeline through its own specialty salesforce or strategic marketing partnerships in the United States. Outside the United States, Savara plans to commercialize its products in collaboration with partners that have the resources and infrastructure to successfully commercialize Savara’s innovative therapeutics. |

Overview of AeroVanc

Background on MRSA infection in cystic fibrosis

CF is a genetic disease characterized, in part, by the prevalence of thick, sticky mucus produced in the lung, frequent lung infections, and a resultant decline in pulmonary function. As the disease progresses, patients’ lungs are typically infected with bacteria that are difficult to eradicate. Inhaled antibiotics, including tobramycin (TOBI, Novartis AG), and aztreonam (Cayston, Gilead Sciences), have become a cornerstone of the treatment of the most common chronic pathogen, Pseudomonas aeruginosa, in order to control the infection and improve lung function and quality of life. In recent years, MRSA lung infection has become increasingly common in CF, with a prevalence of 26 % according to the most recent (2015) data report of the Cystic Fibrosis Foundation. Importantly, persistent MRSA lung infection has been associated with worse clinical outcomes in CF, including a faster decline of lung function1 and a shorter life expectancy.2 The increasing prevalence and high clinical impact of MRSA infection in CF have created an unmet need for improved therapies to help address the condition. Considering the established practice of treating chronic Pseudomonas aeruginosa infection in CF using inhaled

| 1 | Dasenbrook EC, Merlo CA, Diener-West M, et al. “Persistent Methicillin-resistant Staphylococcus aureus and Rate of FEV1 Decline in Cystic Fibrosis.” Am J Respir Crit Care Med 2008;178, 814-821. |

| 2 | Dasenbrook EC, Checkley W, Merlo CA, et al. “Association Between Respiratory Tract Methicillin-Resistant Staphylococcus aureus and Survival in Cystic Fibrosis.” JAMA 2010;303, 2386-2392 |

12

Table of Contents

antibiotics, all of which have limited activity against MRSA, it would be logical to attempt treatment of chronic MRSA infection with an inhaled antibiotic active against MRSA. Savara believes that AeroVanc is the first inhaled antibiotic being developed to specifically treat MRSA infection of the lungs.

Current MRSA treatment options in CF

Persistent MRSA lung infection in CF patients is difficult to eradicate or manage using oral or IV antibiotics, and there is currently no standard of care to manage the infection in CF patients despite the high need.3 In contrast to the established treatment of Pseudomonas aeruginosa infection with inhaled antibiotics, there is no FDA-approved inhaled antibiotic treatment available for MRSA infection.

IV vancomycin or linezolid are the most commonly used drugs for the treatment of acute pulmonary exacerbation in CF patients with MRSA infection, and they may be used in combination with other IV antibiotics in patients with simultaneous Gram-negative infections, such as Pseudomonas aeruginosa. For MRSA lung infection, vancomycin is available only in IV form, and while highly effective against MRSA and other Gram-positive bacteria, chronic home-based use of IV vancomycin is not practical, and chronic use has also been associated with systemic toxicity, especially renal toxicity and ototoxicity.

According to research conducted by Savara, there is increasing clinical need to treat chronic MRSA infection in CF. In the absence of an inhaled antibiotic, there is emerging use of oral anti-MRSA antibiotics in an attempt to suppress the MRSA infection, and in hope of reducing the occurrence of acute pulmonary exacerbations. In a survey conducted by Savara, 27 % of the surveyed CF specialists in the US regularly utilize antibiotics targeting MRSA as a suppressive treatment (any dosage form) in patients with frequent exacerbations or other symptoms for which MRSA is considered a cause or contributing factor. This practice is emerging despite the absence of established consensus or guidelines relating to the use of oral anti-MRSA antibiotics in CF, or evidence of efficacy established in controlled studies.

As with current inhaled anti-pseudomonal drugs, Savara believes that there is significant clinical advantage in delivering an anti-MRSA antibiotic, such as vancomycin, directly to the site of infection to maximize the clinical efficacy, reduce systemic exposure and the risk of adverse effects, and to enable convenient use of the product outside of the hospital setting. The aerosolized IV form of vancomycin, administered by nebulization, has been used in multiple small published clinical studies, mainly to treat ventilator-associated pneumonia in an intensive care setting. In these studies and case reports, nebulized vancomycin had good antibacterial efficacy and was generally well tolerated. In recent years, according to interviews conducted by Savara, many of the leading CF centers in the United States have explored the use of inhaled vancomycin to treat MRSA infected CF patients on a chronic basis, by nebulizing the IV form of vancomycin. The experience gained from this type of treatment has been encouraging, and provides anecdotal reports of the safety and clinical utility of inhaled vancomycin for periods exceeding many years in some patients. Similarly, in the 1990’s, nebulized IV tobramycin was explored as a treatment of Pseudomonas aeruginosa infections in CF patients. This experience stimulated the development of TOBI®, which has become the most widely used inhaled antibiotic worldwide, and a cornerstone of chronic treatment of Pseudomonas aeruginosa lung infection in CF.

Savara believes that inhaled antibiotics, as well as other palliative treatments, will continue to have a central role in the management of CF. Various disease modifying drugs, such as CF Transmembrane Conductance Regulator (CFTR) modulators, that attempt to address the underlying cause of CF, i.e. to restore or improve the function of the CFTR protein that is defective or dysfunctional in CF patients, have recently been launched. Whereas these disease-modifying drugs on average result in modest improvement in lung function and potentially slower rate of lung function decline, patients on these drugs continue to have chronic infections that require antibiotic treatment, and their lung function continues to decline.

| 3 | Zobell JT, Epps KL, Young DC, Montague M, Olson J, Ampofo K, Chin MJ, Marshall BC, Dasenbrook E. “Utilization of antibiotics for methicillin-resistant Staphylococcus aureus infection in cystic fibrosis.” Pediatric Pulmonology (June 2015) Volume 50, Issue 6, pages 552–559 |

13

Table of Contents

AeroVanc Product Description

AeroVanc, or Vancomycin Hydrochloride Inhalation Powder, is a novel inhaled formulation of vancomycin being developed for the treatment of persistent MRSA lung infection in patients with CF. Vancomycin is a glycopeptide antibiotic that was discovered in the mid-1950’s and is commonly used in the prophylaxis and treatment of infections caused by Gram-positive bacteria. Vancomycin acts by inhibiting proper cell wall synthesis of aerobic and anaerobic Gram-positive bacteria, and is generally not active against Gram-negative bacteria.

AeroVanc consists of a capsule dosage form containing a proprietary dry powder formulation of vancomycin hydrochloride intended for oral inhalation with the AeroVanc inhaler. The AeroVanc inhaler is a commercialized, hand-held, manually operated, breath-activated device.

Savara anticipates that AeroVanc will be used predominantly to suppress chronic MRSA lung infection, which has the potential to improve patients’ lung function and respiratory symptoms, and to prolong the time to pulmonary exacerbation and need of systemic antibiotics. AeroVanc is not intended to replace IV vancomycin or other IV antibiotics in the treatment of acute pulmonary exacerbations associated with MRSA. However, chronic AeroVanc use has the potential to reduce the occurrence of these exacerbations, and thereby the need for IV treatments and hospitalizations.

Savara believes there will be broad adoption of AeroVanc in CF once available based on a high level of interest for the product from direct clinician surveys, as well as market research of key opinion leaders in the field of CF. Notably, a clear majority (94 %) of the surveyed CF physicians in the United States would expect to prescribe AeroVanc to their patients with MRSA lung infection, if approved by the FDA. Likewise, according to payer interviews conducted in the United States, an AeroVanc launch would receive reimbursement support given the high unmet need in an orphan indication and a current lack of comparable products.

Clinical Development of AeroVanc

Phase 3

Savara intends to initiate a Phase 3 clinical study designed to demonstrate the safety and efficacy of AeroVanc in CF patients with persistent MRSA lung infection. The plan is to initiate this trial in the third quarter of 2017. The study is planned to be conducted primarily in the United States and Canada.

Savara has received detailed guidance from the FDA on the design of the study, and believes that the planned study is in accordance with the FDA’s requirements for a sole pivotal study to be used in an NDA submission. The study has also been planned in consultation with the Cystic Fibrosis Foundation’s Therapeutic Development Network. The Phase 3 study is designed to detect whether the administration of AeroVanc results in a significant improvement in lung function. The study will assess a 32 mg dose administered twice a day for three on/off cycles of 28 days. The planned primary efficacy endpoint is absolute change from baseline in FEV1 percent predicted, a commonly used measure of lung function. Other efficacy endpoints include the time to use of other antibiotics for pulmonary infection, and a respiratory symptom score.

The planned Phase 3 study is a randomized (1:1), double-blind, placebo-controlled study of AeroVanc in approximately 200 CF patients with persistent MRSA lung infection. The plan is to enrich the study with younger patients, by enrolling 75 % of the subjects between the ages of 6 and 21 years. This was the population most responsive to treatment in the Phase 2 study, and will form the primary analysis population of the study. The duration of the study drug (AeroVanc or placebo) administration will be three cycles of 28 days on drug and 28 days off drug, during which time the primary efficacy endpoint will be measured and assessed. Following the efficacy study period, subjects will transition into another three cycles (28 days on treatment, 28 days off treatment per cycle) of open label AeroVanc use to provide more information on long-term safety.

14

Table of Contents

The planned primary efficacy endpoint of the study is the mean absolute change from baseline in FEV1 percent predicted. In accordance with guidance from the FDA, the endpoint will be analyzed sequentially at Week 4 (first treatment cycle), and at Week 20 (third treatment cycle). Both time points will be tested at a statistical significance level of p = 0.05 due to the sequential nature of the analysis. Savara believes that a statistically significant improvement at Week 20 would provide support for a chronic treatment label, whereas improvement at Week 4 only may result in a more restricted label. Approval in any form is subject to the positive evaluation of the clinical meaningfulness of the treatment effect, judged by the review of all data, including safety data, and the outcome of key secondary endpoints, such as time to use of other antibiotics.

In the single-cycle Phase 2 study, with missing data imputed using conservative rules adopted by the FDA, a difference in the mean absolute change in FEV1 percent predicted of 4.3 % was observed between the treatment arms in subjects below 21 years of age. Based on the observed treatment effect size and variability, a sample size of 45 subjects per arm would provide 90 % power to detect a statistically significant difference at an alpha level of 0.05. To account for a potential loss of power caused by premature discontinuations in a three-cycle study, a sample size of 75 subjects per arm will be enrolled.

Selection of the dose for the study was made based on the Phase 2 study in CF patients. In that study, administration of the 32 mg bid dose resulted in sputum trough vancomycin concentrations that were on average more than 100-fold above the observed minimum inhibitory concentration (MIC90) value, suggesting that the concentrations reached after repeated administration of the 32 mg bid dose are likely to be sufficient for effective management of MRSA infection. In terms of safety and tolerability, the 32 mg AeroVanc dose did not appear significantly different from placebo, and produced encouraging trends of efficacy in all key endpoints in subjects below 21 years of age. In contrast, the higher AeroVanc dose of 64 mg bid was not as well tolerated in the older subjects (above 21 years of age), resulting in an increased number of premature discontinuations of the study drug treatment in this subgroup.

After the completion of the Phase 3 study, Savara intends to submit an NDA applying the 505(b)(2) regulatory pathway. In addition to being designated an Orphan Drug Product and QIDP, AeroVanc has been designated a Fast Track development program by the FDA.

Completed Clinical Studies

Phase 1

In a Phase 1 single escalating dose study, AeroVanc was shown to be generally well tolerated and safe, with a favorable pharmacokinetic profile. In the study, AeroVanc inhalation powder was administered to 18 healthy volunteers (doses of 16 mg, 32 mg, and 80 mg), and seven patients with CF (doses of 32 mg, and 80 mg). AeroVanc demonstrated a relatively slow pulmonary absorption phase (tmax of 1.33 h — 2.08 h), followed by distribution and elimination comparable to IV administration. The mean absolute bioavailability across all AeroVanc doses was 49 % (SD 8 %), with no apparent differences observed between the doses. The absolute bioavailability closely corresponds with the pulmonary absorption of vancomycin, considering that vancomycin is not absorbed from the gastrointestinal tract. The mean Cmax of AeroVanc after an 80 mg dose was 618 ng/mL, corresponding to approximately one fifth of the dose adjusted Cmax after a 250 mg dose of IV vancomycin. The dose linearity of AeroVanc in terms of Cmax and AUC values was excellent (R2 > 0.99). In the CF patients, all subjects had sputum vancomycin concentrations in high excess of the minimum inhibitory concentration, or MIC, of vancomycin for MRSA (2 µg/mL) at one hour after the administration of AeroVanc with both the 32 mg and the 80 mg dose (mean of 106 µg/mL, and 261 µg/mL, respectively). At later time points, the concentrations decreased, but on average remained above the MIC values for up to 24 hours. Variability in sputum concentrations was high, as expected.

All adverse events in the healthy volunteers were classified as mild, and all events that were considered probably drug-related involved local irritation effects and resolved spontaneously and rapidly (between 15 and 60 minutes).

15

Table of Contents

Small reduction in the post-dose FEV1 (7 % — 11 %) was observed in three subjects after the 80 mg dose. None of the subjects required bronchodilator treatment, and the changes were considered by the independent Drug Safety Monitoring Board to be clinically non-significant. In CF patients, chest congestion and/or chest tightness were reported by four of the seven patients, and there appeared to be a slight trend towards more adverse events at the higher dose (80 mg). All reported respiratory adverse events were mild, none of the patients felt distressed, and the events either did not require treatment or resolved after airway clearance and/or albuterol inhalation. Based on the sputum concentration data, dose levels of 32 mg and 64 mg twice a day were selected for use in the Phase 2 study.

Phase 2

In a Phase 2 clinical study in CF patients with persistent MRSA lung infection, AeroVanc met a primary endpoint to reduce MRSA density in sputum, and showed encouraging trends of improvement in lung function, prolongation of the time to use of other antibiotics, and respiratory symptoms, with best responses in subjects below 21 years of age. Savara believes that the consistency of the responses across the different endpoints, as well as the magnitude of change in the younger subjects, supports advancing the product into a Phase 3 clinical study. The results of the Phase 2 study have been summarized and presented to the FDA in an End of Phase 2 Meeting, and the FDA has subsequently given Savara detailed guidance on the design and analysis of a Phase 3 study, as presented above in section “Phase 3”. The key findings of the Phase 2 study are described below.

The study was a randomized, double-blind, placebo-controlled study in 87 CF patients with persistently positive MRSA culture from their sputum samples. The Phase 2 study consisted of a 28-day AeroVanc treatment at a dose level of 32 mg bid or 64 mg bid, with an eight-week follow-up. The study was conducted at 40 sites in the United States. Quantitative MRSA cultures from spontaneously expectorated sputum samples were used as the primary endpoint of the study. The average baseline values in both active drug cohorts, as well as the placebo cohorts were high, ranging from 6.78 to 7.65 log10 CFU/mL. In the primary endpoint analyses (MITT population), a reduction from baseline in MRSA CFU was observed in the 32 mg and 64 mg dose cohorts pooled compared to placebo by -0.52 log10 CFU/mL and -0.06 log10 CFU/mL for the AeroVanc and placebo doses, respectively (p = 0.0312); in the 64 mg dose cohort by -0.63 log10 CFU/mL and 0.16 log10 CFU/mL for the AeroVanc and placebo doses, respectively (p = 0.0145); in the 32 mg dose cohort by -0.25 log10 CFU/mL and -0.30 log10 CFU/mL for the AeroVanc and placebo doses, respectively (p = 0.8352).

MICs of vancomycin for MRSA cultured from the sputum samples were determined using a broth microdilution technique at baseline, at each visit during the administration of AeroVanc, as well as at the post-administration follow-up time points. The distribution of MIC values was very narrow, with the MIC50 and MIC90 both at 0.5 µg/mL at baseline. At baseline, all strains were susceptible to vancomycin, with MIC values £ 1 µg/mL, and there were no notable changes in the MIC distribution at any of the time points following the baseline sample, suggesting the susceptibility of MRSA to vancomycin was not affected by the 28 days of pulmonary administration of AeroVanc.

As illustrated in the graph below, vancomycin peak and trough concentrations in sputum at Day 8 and Day 29 were in high excess over the generally accepted level of MIC (mean Ctrough/MIC ratio > 35) after multiple dosing in all subjects at both dose levels, with apparent dose-dependency, but no notable difference in Ctrough between the two time points. The generally accepted MIC of vancomycin for MRSA is illustrated below by the dotted line, at 2 µg/mL.

16

Table of Contents

Vancomycin sputum concentrations after administration of AeroVanc at various time points

In terms of safety, the most frequent adverse events reported were related to the respiratory system. The AeroVanc 32 mg bid dose was well tolerated, with no significant difference in adverse events as compared with placebo. However, a higher incidence of adverse events, most frequently consistent with signs and symptoms of bronchoconstriction, and a significantly higher rate of premature study drug discontinuations were seen in adult patients with the 64 mg bid AeroVanc dose, as compared with placebo and the 32 mg AeroVanc dose. The discontinuations were most commonly reported to be due to drug intolerability (mainly bronchoconstriction and/or chest tightness) or pulmonary exacerbation, and typically occurred within the first two weeks from the start of drug administration.

Based on the observed clinical results in the 32 mg cohort of subjects below 21 years of age, the observed high vancomycin concentrations in sputum at both dose levels, and the high discontinuation frequency in adult subjects at the 64 mg dose, the Phase 3 study is planned to be conducted using the 32 mg dose, and will focus enrollment on subjects below 21 years of age. Accordingly, the key Phase 2 data from this cohort, below 21 years of age, are summarized below.

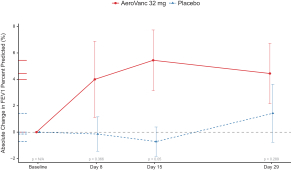

To assess effects of AeroVanc on lung function, absolute change in FEV1 percent predicted from baseline was measured at each study visit. While AeroVanc reduced MRSA density in sputum, the change in FEV1 compared with placebo did not reach statistical significance in subjects of all ages. Notably, post hoc analyses identified encouraging improvement in FEV1 in subjects 21 years of age or younger, consistently across all time points during the treatment period, as illustrated below. The mean absolute change in FEV1 percent predicted observed in the AeroVanc arm is considered clinically meaningful, with an improvement ranging between 4 % and 6 % (or 6 % and 10 % on a relative change basis). In this subgroup, the difference between AeroVanc and placebo was statistically significant at the 2-week time point (p = 0.05). A mean reduction of 0.8 log10 CFU/mL from baseline in MRSA CFUs, the primary endpoint, was also observed after 28 days of AeroVanc administration in subjects below 21 years of age, as illustrated below, the difference between AeroVanc and placebo being statistically significant (p = 0.05).

17

Table of Contents

Change from baseline in FEV1

(Per Protocol Population, 32 mg dose cohort, below 21 years of age, n = 16)

These results are consistent with previous studies using inhaled tobramycin (TOBI® or TOBI Podhaler®) for the treatment of P. aeruginosa infection in CF, where improvement in FEV1 was predominantly seen in younger subjects4. In the early TOBI trials, reported in the 1990’s, during an era when the use of inhaled antibiotics was not yet prevalent, children and adolescents (below 18 years of age) showed relative improvements of greater than 14 % as compared with only 6 % in adults5. However, in more recent studies, reported in 2012, the relative FEV1 improvements have been considerably smaller, either being absent or less than 2 % in adults.6

As illustrated below, a mean reduction of 0.8 log10 CFU/mL from baseline in MRSA CFUs, the primary endpoint, was observed after 28 days of AeroVanc administration in subjects below 21 years of age, the difference between AeroVanc and placebo being statistically significant (p = 0.05).

| 4 | Weers J. “Inhaled antimicrobial therapy – Barriers to effective treatment. Advanced Drug Delivery Reviews.” (2015): 24-43. |

| 5 | Ramsey BW, Pepe MS, Quan JM, Otto KL, Montgomery AB, Williams-Warren J, Vasiljev-K M, Borowitz D, Bowman CM, Marshall BC, Marshall S, Smith AL. “Intermittent administration of inhaled tobramycin in patients with cystic fibrosis. Cystic Fibrosis Inhaled Tobramycin Study Group.” New England Journal of Medicine. 1999 Jan 7;340(1):23-30. |

| 6 | TOBI Podhaler SBA; NDA-201688, 2012 |

18

Table of Contents

Change in MRSA density in sputum

(Intent-to-treat Population, 32 mg dose cohort, below 21 years of age, n = 20)

A greater reduction in CFRSD-CRISS, the respiratory symptom score, was observed in the below 21-year age group consistently at all time points, as compared with placebo, but the difference was not statistically significant.

A trend of prolongation of the time to use of another antibiotic for respiratory symptoms was observed in the AeroVanc arm of the 32 mg dose cohort, as compared with placebo, illustrated below. Whereas in this single cycle study several subjects in the AeroVanc arm were prescribed other antibiotics at the scheduled one-month post-treatment visit (approximately Day 56), such treatment would not be expected to be prescribed during chronic AeroVanc treatment, or in a multiple-cycle study, because the timing would coincide with the start of a new AeroVanc treatment period.

19

Table of Contents

Time to use of other antibiotics for respiratory infection

(Intent-to-treat Population, 32 mg dose cohort, below 21 years of age, n = 20)

In summary, AeroVanc reduced MRSA density in sputum, and showed encouraging trends of improvement in lung function, prolongation of the time to use of other antibiotics, and respiratory symptom, with best responses in subjects below 21 years of age. Savara believes that the consistency of the responses across the different endpoints, as well as the magnitude of change in the younger subjects, supports advancing the product into a Phase 3 clinical study.

Human factor study

Savara has performed a human factor study to better understand patient reactions to the AeroVanc inhaler device, the drug capsule and written instructions. 14 CF patients, representing a variety of sex, ethnicity and dominant hand preference and ranging in age from 12 to 56 years participated in the study. Patients were given the device, capsules and instructions to simulate use (no drug) and provide feedback. In summary, all patients were able to use the device properly and no device design issues were identified that could impact proper use.

Overview of Molgradex

Background on PAP

PAP is a rare lung disease, which affects up to seven out of a million people in the United States7, and has a similar prevalence in Japan8. PAP is characterized by the build-up of lung surfactant in the alveoli, or air sacs, of

| 7 | Trapnell BC, Avetisyan R, Carey B, Zhang W, Kaplan P, Wang H. Prevalence of pulmonary alveolar proteinosis (PAP) determined using a large health care claims database. Am J Respir Crit Care Med. 2014;VOL:abstract A6582. |

| 8 | Inoue Y, Trapnell BC, Tazawa R, Arai T, Takada T, Hizawa N et al. Characteristics of a large cohort of patients with autoimmune pulmonary alveolar proteinosis in Japan. Am J Respir Crit Care Med 177: 752–62, 2008 |

20

Table of Contents

the lungs. The surfactant consists of proteins and lipids, and is an important physiological substance that coats the inside of the alveoli to prevent the lungs from collapsing. The lungs continuously produce new active surfactant. In a healthy lung, the old and inactivated surfactant is cleared and digested by immune cells called alveolar macrophages. In PAP lungs, however, the macrophages fail to clear the surfactant from the alveoli, leading to gradual accumulation of excess surfactant in the alveoli. The root cause of PAP is an autoimmune response against a naturally occurring protein of the body, GM-CSF. Pulmonary macrophages need to be stimulated by GM-CSF to function properly, but in autoimmune PAP, GM-CSF is deactivated by antibodies against GM-CSF, rendering the macrophages unable to perform their tasks, such as clearing the surfactant from the alveoli.

PAP commonly affects men in early middle age, but both sexes and subjects of any age can be affected. As a result of the accumulation of excess surfactant, gas exchange in the lungs is obstructed, and patients start to experience shortness of breath, and decreased exercise tolerance. Shortness of breath is typically first observed upon exertion, but as the disease progresses, also at rest. Patients may experience chronic cough, as well as episodes of fever, chest pain, or coughing blood, especially if secondary lung infection develops. In the long term, the disease can lead to serious complications, including lung fibrosis and the need for lung transplant. Mortality due to PAP has decreased over the last decades with better clinical management, but in rare cases serious lung infections or respiratory insufficiency may lead to death.

Current treatment options of PAP

The current standard of care for PAP is a procedure called whole lung lavage, or WLL, which entails washing out the lungs with saline under general anesthesia. WLL is an invasive and inconvenient procedure that requires highly experienced physicians at specialist sites. The procedure in conducted in an operating room, thereby requiring hospitalization, and admission to intensive care after the procedure. In many patients, WLL only provides temporary symptomatic relief, and once the lungs refill with surfactant, the WLL procedure needs to be repeated.

As there are no approved drug treatments available for PAP, Savara believes there is a high need for a convenient and efficacious medicinal treatment. Savara believes that inhalation of GM-CSF directly into the lungs has the potential to replace the inactivated GM-CSF, and thereby to restore the surfactant clearing activity of the alveolar macrophages. As a result, Savara believes that inhaled GM-CSF has the potential for considerable improvement in oxygenation and exercise tolerance. An injectable form of GM-CSF, sargramostim (Leukine®, Sanofi-Aventis), is approved and on the market in the United States for IV and subcutaneous administration for the treatment of neutropenia caused by cancer chemotherapy, but there is currently no inhalation formulation of GM-CSF available.

The potential benefits of inhaled GM-CSF in PAP, together with the availability of sargramostim, have stimulated independent clinicians and academic researchers in the United States, Europe, and Japan to study the safety and efficacy of GM-CSF, administered by inhalation, in PAP patients. Several such investigator-sponsored open-label clinical studies and case studies of inhaled GM-CSF treatment have been published, with promising results on the efficacy and safety of the treatment.9,10,11 In total, treatment of more than 80 PAP patients with

| 9 | Tazawa R, Trapnell BC, Inoue Y, Arai T, Takada T, Nasuhara Y, et al. Inhaled Granulocyte/Macrophage–Colony Stimulating Factor as Therapy for Pulmonary Alveolar Proteinosis. Am J Resp Crit Care Med 181: 1345-1354, 2010 |

| 10 | Wylam ME, Ten R, Prakash UB, Nadrous HF, Clawson ML and Anderson PM (2006). Aerosol granulocyte-macrophage colony-stimulating factor for pulmonary alveolar proteinosis. Eur Respir J 27(3): 585-93 |

| 11 | Papiris SA, Tsirigotis P, Kolilekas L, Papadaki G, Papaioannou AI, Triantafillidou C, et al. (2014). Long-term inhaled granulocyte macrophage-colony-stimulating factor in autoimmune pulmonary alveolar proteinosis: effectiveness, safety, and lowest effective dose. Clin Drug Investig 34(8): 553-64 |

21

Table of Contents

inhaled GM-CSF has been reported in open-label studies or retrospective cohorts, as well as several individual case reports. Whereas the majority of the patients described in the literature received sargramostim, the results indicate that both sargramostim and molgramostim have the potential for a very positive impact on oxygenation and clinical symptoms in PAP patients.

According to Savara’s review of published literature, few safety issues related with molgramostim or sargramostim inhalation in patients with PAP have been reported. However, there is still limited information available on the long-term safety of inhaled GM-CSF. In indications other than PAP, more than 100 patients, mainly with a cancer diagnosis, have received inhaled sargramostim, in doses up to 4000 µg/day. Pulmonary toxicity was the most frequently reported toxicity at high doses. An increase in both number and severity of adverse events with increasing dose has been observed. However, due to the underlying diseases it was often difficult for the investigators to assess causality of the adverse event cases.

Molgradex Product Description

Molgradex is a novel inhaled formulation of recombinant human GM-CSF being developed for the treatment of PAP. The active drug substance, molgramostim, is a non-glycosylated form of GM-CSF. GM-CSF is an endogenous growth factor that stimulates the proliferation and differentiation of hematopoietic cells (blood and immune cells), mainly granulocytic and monocytic cell lines, which serve as the body’s first line of defense against bacteria and viruses, and also function to clear cellular debris and waste substances from the body. Molgramostim is produced in a strain of Escherichia coli bearing a genetically engineered plasmid containing a human GM-CSF gene.

Molgradex, is a sterile nebulizer solution in a vial containing 300 µg of molgramostim, designed to be administered once daily by inhalation via a high efficiency nebulizer (Investigational eFlow Nebuliser System, PARI Pharma GmbH, Germany). The PARI eFlow Nebulizer system for use with investigational drug products is a reusable electronic inhalation system that has been optimized for administration of Molgradex.

Savara anticipates that Molgradex will be used as a long-term therapy in patients with PAP. The optimal duration of treatment is currently not known, and is likely to vary between patients depending on the disease severity and the natural course of their disease. Molgradex treatment may not entirely eliminate the need for WLL in all patients, but based on interviews conducted by Savara, PAP centers that have experimented with long-term inhaled GM-CSF have seen a considerable reduction of WLL procedures.

Molgradex was granted Orphan Drug Designation by the FDA in October, 2012, and by EMA in July, 2013, for the treatment of PAP. Safety and tolerability of inhaled Molgradex has been tested in a Phase 1 clinical study in 42 healthy human volunteers. Safety and efficacy of inhaled Molgradex in PAP patients is currently being tested in a Phase 2/3 clinical study in up to 51 PAP patients. Since 2014, Molgradex has been available in several European countries for the treatment of PAP for named patients following unsolicited physician requests.

Clinical Development of Molgradex

Phase 2/3

Savara is currently conducting a Phase 2/3 clinical study on Molgradex in Europe and Japan in PAP patients. Based on the scientific advice received from the EMA, Savara believes the study has the potential to be accepted as the sole pivotal study in support of a marketing authorization application in the European Union. The aim of this randomized, double-blind, placebo-controlled study is to compare efficacy and safety of Molgradex with placebo in up to 51 PAP patients. In the study, Molgradex 300 µg is administered once daily for up to 24 weeks, with a follow-up period up to 48 weeks.

Patients diagnosed with autoimmune PAP and fulfilling all other entry criteria are randomized to receive double-blind treatment for up to 24 weeks in one of three treatment arms: 1) Molgradex 300 µg administered

22

Table of Contents

once daily, 2) Molgradex 300 µg and matching placebo administered daily in 7-day intermittent cycles of each, or 3) inhaled placebo administered once daily. The study is conducted at multiple sites in the European Union, Russia, Israel and Japan.

The primary endpoint is the absolute change from baseline of arterial-alveolar oxygen gradient ((A-a)DO2) after 24 weeks of treatment. This endpoint is a measure of patient’s oxygenation status, and the endpoint value is expected to decrease as the physical obstacle of gas exchange is reduced by clearance of excess surfactant from the lungs. Key secondary endpoints assessed after 24 weeks of treatment include the number of patients in need of WLL during 24-week treatment, as well as change in the vital capacity of the lungs after 24-week treatment.

Based on the sample size calculation for the study, 42 evaluable patients (14 in each treatment group) are required to be randomized to have 90 % power to detect a difference of 10 mmHg in A-a(DO2) between the two active arms combined and placebo, using a significance level of 0.01. To account for potential study discontinuations or non-evaluable patients, a total of up to 51 patients is planned to be randomized.

A data safety monitoring board, or DSMB, provides safety oversight in the Phase 2/3 study. Following its first meeting in October, 2016, no concerning safety issues were identified and the DSMB endorsed continuation of the study as planned.

Savara has conducted a Type C meeting with the FDA to seek guidance on the nonclinical and clinical requirements for an NDA submission in the United States. The FDA acknowledged that a single Phase 3 study may potentially be sufficient to support approval of Molgradex for treatment of PAP, provided that it demonstrates persuasive evidence of efficacy across clinically meaningful endpoints. Whereas the current study design and sample size of the IMPALA study may not be acceptable to the FDA as a sole pivotal study, the FDA gave initial guidance on modifications of the study that could potentially make it acceptable as the sole study for NDA submission and approval. Savara will diligently continue its interaction with the FDA in order to reach agreement on the clinical program structure and details, and targets to complete the negotiations by the end of the third quarter of 2017. The final outcome may involve the amendment of the IMPALA study to serve as a sole pivotal study, or the conduct of a separate pivotal clinical study prior to submitting an NDA.

Completed Clinical Studies

Phase 1

In a Phase 1 Molgradex study in 42 healthy adult volunteers, the drug was generally well tolerated and produced dose-dependent increases in total and differential white blood cell (WBC) counts consistent with the known pharmacologic effect of GM-CSF. The study was a randomized, double-blind, placebo-controlled, single ascending dose (SAD) and multiple ascending dose (MAD) study to assess the safety, tolerability, pharmacokinetics, and pharmacodynamics of Molgradex. In the SAD part, 18 subjects were included with four subjects in each of the three SAD dose levels (150 µg, 300 µg and 600 µg) and six subjects received placebo. In the MAD part, 24 subjects were included with nine subjects in each of the two MAD dose levels (300 µg or 600 µg) and six subjects received placebo for six days.

In the SAD part, GM-CSF was absorbed into the systemic circulation with a tmax of two hours after inhalation of Molgradex, however, at picogram levels, 50 to 100 times lower than has been observed after similar doses of GM-CSF administered intravenously. Total systemic exposure (AUClast) increased with dose, ranging between 13 and 138 pg•h/mL and maximum concentration (Cmax) ranging between 9.1 and 41 pg/mL (Cmax was similar for the 300 and 600 µg dose levels). In the MAD part, there was evidence of some accumulation after multiple dosing; Cmax increased from 32 pg/mL on Day 1 to 90 pg/mL on Day 6 at the 300 µg dose, and from 96 pg/mL on Day 1 to 251 pg/mL on Day 6 at the 600 µg dose level. Likewise, AUClast increased from 97 to 248 pg•h/mL from Days 1 to 6 for the 300 µg dose level and from 350 to 802 pg•h/mL for the 600 µg dose level. Minimum measurable plasma concentrations (Cmin) on Day 6 were 3.6 and 5.1 pg/mL measured at 8 and 12 hours, respectively for the 300 and 600 µg dose levels.

23

Table of Contents

In subjects treated with Molgradex, a slight increase in total WBC and differential counts (primarily within normal reference ranges) was observed in a dose-dependent manner, in-line with the known biological mode-of-action of GM-CSF, as illustrated in the graph below.

Mean WBC Over Time and After Multiple Ascending Doses

The primary aim of the Phase 1 study was to assess the safety and tolerability of Molgradex. No meaningful difference in the frequency or severity of AEs was observed between Molgradex 300 µg and placebo. The most common AE was cough, reported in 21 out of 30 (70 %) subjects receiving Molgradex and 8 out of 12 (67 %) patients receiving placebo, and there was no difference in the causality assessment between the treatment arms. A higher number of treatment-related AEs were observed at the 600 µg dose compared to the 300 µg dose and placebo in the MAD part. There were no serious or severe adverse events, dose-limiting toxicity or other remarkable findings of clinical concern in the safety data.

Nonclinical Studies

AeroVanc Inhalation Toxicology Studies

The nonclinical toxicology profile of AeroVanc has been characterized in a series of acute and repeated dose inhalation toxicity studies in rats and dogs, as well as ICH/FDA prescribed safety pharmacology studies involving the cardiovascular, pulmonary, and central nervous systems. In these studies, a gradation of dose levels, including the maximum tolerated dose or the maximum technically achievable dose, were evaluated in both species.

24

Table of Contents

Following 28 days of inhalation exposure, there were no indications of systemic toxicity noted in either the rats or dogs. As expected, there were a number of microscopic changes noted along the respiratory tract and in the lungs that were considered to represent local irritative effects, adaptive changes, and normal physiological responses to the impaction of particles along the respiratory tract and deposition of particles in the lungs. A 28-day recovery period showed complete to partial reversibility of the findings, with no notable difference between the active dose groups and the vehicle control group when compared to the air control. Based on the results of these 28-day studies, the No Observed Adverse Effect Level (NOAEL) was established for both species, and AeroVanc was considered safe for the purpose of conducting the Phase 2 study.

After completion of the Phase 2 clinical study, Savara received guidance from the FDA regarding the necessary toxicology studies to support the planned Phase 3 study and NDA submission. In accordance with the FDA’s guidance, a 91-day inhalation toxicology study was conducted in rats. Savara believes that the NOAEL established in this study supports the proposed Phase 3 study with the intended dose level.

A two-year GLP inhalation carcinogenicity study of AeroVanc in rats is mandated by the FDA prior to submission of an NDA. The purpose of this study is to determine whether lifetime pulmonary exposure to AeroVanc at high doses may result in any gross or microscopic indications of neoplasia in rats. The 91-day inhalation toxicology report and the carcinogenicity study protocol have been evaluated by the FDA Carcinogenicity Assessment Committee (CAC) in a Special Protocol Assessment (SPA) to confirm that the study design and dose levels are adequate to meet scientific and regulatory requirements. The CAC has notified Savara of their feedback, which has been considered in finalizing the protocol. The study will be conducted by a specialized contract research organization that has conducted all prior inhalation toxicology studies of AeroVanc, and has the required capabilities and operating procedures in place.

Molgradex Pharmacology Studies

The pharmacology of GM-CSF in the lungs involves stimulation of alveolar macrophage and neutrophil function to maintain alveolar surfactant homeostasis, alveolar stability, lung function, and lung host defense. For example, pulmonary GM-CSF is required for the terminal differentiation of alveolar macrophages and acquisition of numerous functions including expression of multiple receptors, non-specific and receptor-mediated endocytosis and phagocytosis, for pulmonary neutrophil recruitment during infection, clearance of bacteria, viruses, mycobacteria, and other pathogens, as well as for surfactant clearance.

The pharmacodynamics of human GM-CSF receptor activation by Molgradex was determined as part of Savara’s studies of species evaluation and selection for inhalation toxicology and reproductive toxicology studies. As illustrated below, the effective concentration of molgramostim from Molgradex required to stimulate a half maximal receptor signaling response (EC50), as measured by phosphorylation of STAT5, was similar to that of commercially available rhGM-CSF. Thus, Molgradex is expected to possess the expected biological regulatory action of GM-CSF on alveolar macrophages in the lungs.

25

Table of Contents

GM-CSF receptor function by Molgradex or control recombinant human GM-CSF

Further in vitro or in vivo nonclinical studies investigating the pharmacological activity of Molgradex are not planned.

Molgradex toxicology studies

The nonclinical toxicology profile of Molgradex has been characterized in a series of repeated dose inhalation toxicology studies and safety pharmacology studies in cynomolgus monkeys, as well as reproductive toxicology studies in rabbits. In these studies, a gradation of dose levels was evaluated in the respective species.

Three GLP-compliant inhalation toxicology studies were conducted, including a 6-week inhalation toxicity study in young sexually immature monkeys, a 13-week inhalation toxicity study in sexually mature monkeys used to explore effects on male and female reproductive organs, and a 26-week inhalation toxicity study to investigate chronic toxicity. All studies are fully compliant with relevant guidelines from ICH/FDA.

After inhalation of Molgradex, local effects in the lungs were characterized by infiltrating inflammatory cells, mostly macrophages, accompanied by an increased cellularity in the lymphoid tissue that is associated with the respiratory tract and minimal to mild exudation of red blood cells into the alveoli. The infiltration of inflammatory cells was not associated with any other signs of inflammation or impaired lung function, and it was considered an exaggerated pharmacological effect of molgramostim. The severity of the findings was graded slight at the lowest dose level, and moderate above this level. Duration of treatment did not affect the severity of this finding. Reduced severity of the lung and tracheobronchial changes following a four-week recovery period suggested partial resolution of the changes.